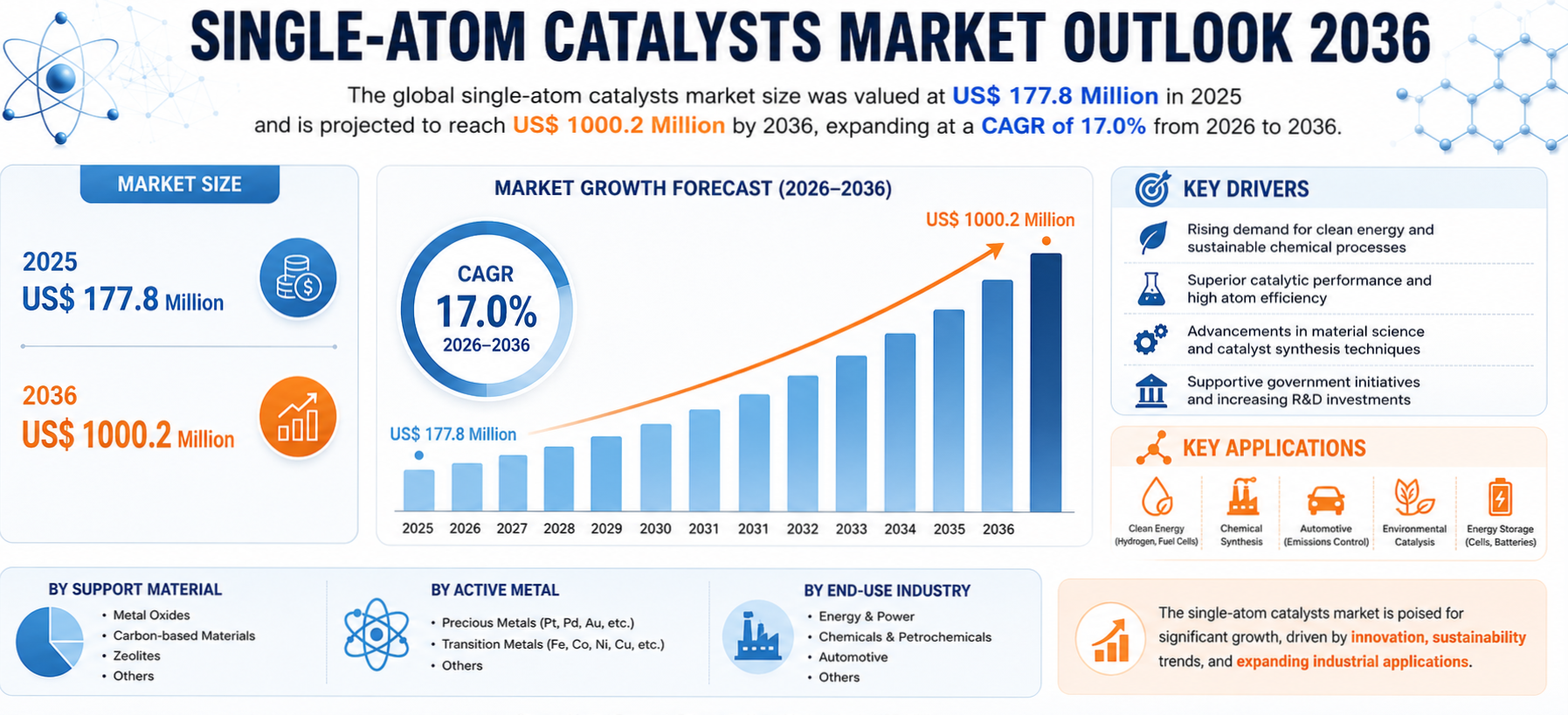

The global single-atom catalysts market is poised for remarkable expansion over the next decade, driven by increasing demand for sustainable catalytic technologies, rapid commercialization of green hydrogen projects, and rising investments in industrial decarbonization. According to recent industry analysis, the global single-atom catalysts market was valued at US$ 177.8 Million in 2025 and is projected to reach US$ 1000.2 Million by 2036, expanding at a robust CAGR of 17.0% during the forecast period from 2026 to 2036.

Single-atom catalysts (SACs) are emerging as one of the most transformative innovations in advanced materials and catalysis technologies. These catalysts consist of isolated metal atoms dispersed on support materials such as carbon, metal oxides, zeolites, or polymers. Unlike traditional nanoparticle catalysts, SACs maximize atomic efficiency, improve reaction selectivity, and significantly reduce precious metal usage.

Access important conclusions and data points from our Report in this sample –

https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86941

The growing urgency for low-carbon manufacturing, emission reduction, and energy-efficient chemical processes is accelerating the adoption of SACs across industries including chemicals, petrochemicals, automotive, energy & power, water treatment, and biomedical applications.

Market Size and Industry Outlook

The single-atom catalysts market is transitioning from a research-centric ecosystem to an early-stage commercialization phase. Industrial players and governments worldwide are increasingly investing in catalyst technologies that enable high efficiency, reduced energy consumption, and lower operational costs.

The market reached a valuation of US$ 177.8 Million in 2025 and is forecast to witness nearly six-fold growth by 2036. This extraordinary growth trajectory reflects the increasing deployment of SACs in fuel cells, hydrogen electrolyzers, environmental catalysis systems, and next-generation chemical synthesis technologies.

One of the most significant advantages of SACs lies in their ability to achieve near 100% utilization of active metal atoms. Conventional catalysts typically utilize only 30-40% of active metal atoms effectively, whereas SACs drastically improve utilization rates while reducing the dependence on expensive precious metals such as platinum, iridium, and palladium.

Studies indicate that SACs can reduce precious metal loading by 50-70% while delivering 2-5 times higher mass activity compared to nanoparticle-based catalysts. These economic and performance advantages are expected to position SACs as indispensable components in future clean energy infrastructure.

Market Overview

Single-atom catalysts represent a major advancement in catalytic science due to their highly controlled active sites and superior selectivity. By atomically dispersing metal atoms on stable support materials, SACs improve catalytic efficiency while minimizing by-product formation and energy losses.

The technology has gained significant traction in applications such as:

- Green hydrogen production

- Fuel-cell systems

- CO₂ conversion

- Environmental emission control

- Chemical synthesis

- Sensors and biomedical applications

Industries are increasingly focusing on sustainable manufacturing technologies that align with global carbon neutrality goals. SACs contribute directly to these objectives by lowering reaction temperatures, improving process selectivity, and reducing waste generation.

Moreover, advancements in thermal stability and atom stabilization technologies have addressed earlier concerns regarding atom migration and catalyst agglomeration, enabling broader industrial adoption.

Asia Pacific currently dominates the global market, accounting for approximately 43% of total market revenue in 2025. The region benefits from strong government support, large-scale hydrogen infrastructure projects, and extensive chemical manufacturing capacity.

Key Market Growth Drivers

Faster Adoption of Green Hydrogen and Fuel-Cell Systems

The rapid growth of green hydrogen projects worldwide is one of the primary factors driving the SACs market. Hydrogen electrolyzers and proton exchange membrane (PEM) fuel cells rely heavily on precious metal catalysts such as platinum and iridium, which contribute significantly to total system costs.

Single-atom catalysts address this challenge by maximizing metal atom utilization and reducing overall catalyst requirements. Research demonstrates that SACs can achieve 2-5 times greater catalytic activity while reducing precious metal usage by as much as 70%.

As governments and private investors allocate billions of dollars toward hydrogen hubs, renewable energy systems, and fuel-cell vehicle infrastructure, demand for cost-efficient catalyst technologies is rising sharply.

Large-scale hydrogen projects exceeding 100 MW capacity require economically viable catalyst systems to ensure long-term scalability and profitability. SACs are increasingly viewed as a critical enabler for affordable green hydrogen production.

Industrial Emissions Control and Electrification-Driven Chemical Manufacturing

Stringent environmental regulations and industrial decarbonization goals are further accelerating SAC adoption. Industries are under growing pressure to reduce NOx emissions, carbon intensity, and operational energy consumption.

Single-atom catalysts improve catalytic efficiency and enhance selectivity, reducing fuel penalties and minimizing process downtime. In chemical manufacturing, SACs can lower reaction temperatures by 20-40°C, resulting in energy savings of approximately 5-10% in continuous production systems.

Additionally, SACs improve product yields by 5-20 percentage points, reducing waste generation and downstream separation costs. These operational advantages are becoming increasingly important as industries transition toward electrified and low-carbon production methods.

Analysis of Key Players – Key Player Strategies

Leading companies operating in the global single-atom catalysts market are actively investing in R&D, pilot-scale manufacturing, strategic collaborations, and catalyst optimization technologies to strengthen their market positions.

Johnson Matthey

Johnson Matthey is leveraging its expertise in precious metal chemistry to develop advanced SAC technologies for fuel cells, electrolyzers, and emissions control systems. The company is focusing on improving catalyst efficiency while reducing precious metal dependence.

Sinopec Catalyst Co., Ltd.

Sinopec benefits from strong integration with China’s refining and petrochemical ecosystem. The company is utilizing extensive R&D capabilities to commercialize SAC technologies for hydrogen production and industrial catalysis applications.

Topsoe

Topsoe is emphasizing sustainable catalysis and green hydrogen technologies. The company is developing atom-efficient catalyst systems to support industrial decarbonization and renewable fuel production.

BASF SE

BASF SE is strengthening its catalyst innovation capabilities through investments in advanced research facilities and pilot-scale catalyst development centers.

Other Major Players

Additional companies contributing to market expansion include:

- MSE Supplies

- Evonik Industries AG

- Clariant AG

- Angstrom Advanced Inc

- Umicore N.V.

- Shanghai Richem International Co., Ltd

- Nanjing Catalyst New Material Co., Ltd

- W.R. Grace & Co

These players are focusing on strategic partnerships, commercialization of next-generation catalysts, and expansion of R&D activities to gain competitive advantages.

Market Challenges and Opportunities

Challenges

Despite strong growth potential, the single-atom catalysts market faces several challenges:

- High initial R&D and commercialization costs

- Complex manufacturing and stabilization processes

- Scalability limitations for large-scale industrial deployment

- Limited standardization across catalyst platforms

- Technical challenges related to long-term thermal stability

The transition from laboratory-scale innovation to industrial-scale commercialization requires substantial capital investment and advanced process engineering capabilities.

Opportunities

The commercialization of SACs in green hydrogen and CO₂ conversion presents substantial opportunities for market participants.

In electrolyzer systems, SACs can significantly lower precious metal requirements, improving project economics for large-scale hydrogen facilities ranging from 100 MW to 500 MW.

Similarly, SACs demonstrate superior selectivity in CO₂-to-CO and CO₂-to-methanol conversion pathways. Enhanced selectivity can reduce by-product formation while improving energy efficiency and reactor throughput.

Growing investments in carbon capture, sustainable fuels, and renewable energy infrastructure are expected to create long-term opportunities for catalyst manufacturers and technology developers.

Key Player Strategies

Market participants are implementing several strategic initiatives to strengthen their competitive positions:

- Expanding pilot-scale catalyst manufacturing facilities

- Investing heavily in advanced catalyst R&D

- Developing atom-efficient catalyst platforms

- Collaborating with hydrogen and fuel-cell technology providers

- Enhancing catalyst durability and thermal stability

- Strengthening commercialization pipelines for industrial applications

Companies are also focusing on reducing catalyst costs and improving scalability to accelerate adoption across commercial energy and chemical sectors.

Recent Developments

A study was carried out by Johnson Matthey Plc in 2025, evaluating the application of Single Atom Catalysts (SACs) or Single Atom Alloy (SAA) catalysts for the methanation of CO₂. The study went ahead to conceptualize how alloys could be employed for enhanced selectivity and efficiency of catalysis, a crucial milestone for catalysis.

Johnson Matthey Plc has agreed to the sale of its Catalyst Technologies business to Honeywell International in 2025 for US$ 2.4 Billion. The agreement has implications for the company’s business in the catalyst area, encompassing industrial and process catalysts. The acquisition will help Honeywell diversify its portfolio of catalysts.

In the year 2024, BASF SE launched the opening of its new Catalyst Development and Solids Processing Center in Ludwigshafen, Germany. The new facility enhances the R&D and pilot scales of BASF in the development of novel catalysts. BASF can develop novel materials for catalysts that help in the design of atom-efficient catalysts.

In 2024, MSE Supplies enhanced its market position in the single-atom catalysts market by creating SAC-related technical articles and promoting its existing product range of single-atom catalysts, namely Co-N-C SACs intended for electro-catalysis and thermocatalysis research. The products are meant for research in H2 evolution, O2 reduction reactions, and conversion of CO2. By supplying researchers in universities, labs, and R&D divisions of companies with readily available and well-dispersed SACs, MSE Supplies facilitated quick experimentation and prototyping of the novel catalyst structures.

Investment Landscape and ROI Outlook

The investment outlook for the single-atom catalysts market remains highly favorable due to increasing global spending on clean energy infrastructure, sustainable manufacturing, and carbon reduction technologies.

Governments across Asia Pacific, North America, and Europe are allocating substantial funding toward hydrogen ecosystems, fuel-cell mobility, and advanced catalyst technologies. China alone continues to invest heavily in hydrogen production, advanced materials research, and industrial decarbonization programs.

For investors, SAC technologies offer attractive long-term returns due to:

- Rising demand for green hydrogen systems

- Increasing adoption of fuel-cell technologies

- Expansion of carbon capture and CO₂ utilization projects

- Industrial electrification trends

- Higher operational efficiencies and lower catalyst costs

As commercialization scales up, manufacturers capable of reducing precious metal dependency and improving catalyst stability are expected to generate strong revenue growth and competitive differentiation.

Market Segmentations

By Product Type

- Metal-based

- Non-Metal-based

- Hybrids

- Others

By Support Material

- Carbon-based

- Metal Oxides

- Zeolites

- Polymers

- Others

By Application

- Chemical Synthesis

- Energy Conversion

- Environmental Catalysis

- Sensors

- Drug Delivery

- Others

By End-use

- Chemicals & Petrochemicals

- Automotive

- Energy & Power

- Biomedical

- Electronics

- Water Treatment

- Others

By Region

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East & Africa

Countries Covered

- U.S.

- Canada

- Germany

- U.K.

- France

- Spain

- Italy

- Russia and CIS

- Japan

- China

- India

- ASEAN

- Brazil

- Mexico

- GCC

- South Africa

Why Buy This Report?

- Gain comprehensive insights into the global single-atom catalysts market

- Understand key growth drivers, challenges, and opportunities

- Analyze competitive positioning of major industry participants

- Evaluate emerging trends in green hydrogen and CO₂ conversion

- Access detailed regional and segment-wise market forecasts

- Identify high-growth investment opportunities

- Understand technological advancements shaping the catalyst industry

- Support strategic decision-making with data-driven market intelligence

Frequently Asked Questions (FAQs)

1. What is the projected growth rate of the single-atom catalysts market?

The market is projected to expand at a CAGR of 17.0% from 2026 to 2036.

2. What will be the market size of the single-atom catalysts industry by 2036?

The global market is expected to reach US$ 1000.2 Million by 2036.

3. Which region dominates the single-atom catalysts market?

Asia Pacific currently leads the market with approximately 43% revenue share.

4. What are the major applications of single-atom catalysts?

Major applications include green hydrogen production, fuel cells, environmental catalysis, chemical synthesis, and CO₂ conversion.

5. Which companies are leading the global single-atom catalysts market?

Key companies include Johnson Matthey, Sinopec Catalyst Co., Ltd., Topsoe, BASF SE, Evonik Industries AG, and Umicore N.V.

About Us Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. The firm scrutinizes factors shaping the dynamics of demand in various markets. The insights and perspectives on the markets evaluate opportunities in various segments. The opportunities in the segments based on source, application, demographics, sales channel, and end-use are analysed, which will determine growth in the markets over the next decade.

Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision-makers, made possible by experienced teams of Analysts, Researchers, and Consultants. The proprietary data sources and various tools & techniques we use always reflect the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in all of its business reports.

Media Contact:

Abhishek Budholiya

Transparency Market Research Inc.

State Tower, 90 State Street, Suite 700,

Albany NY – 12207, United States

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Media Inquiries: media@transparencymarketresearch.com

Sales Inquiries: sales@transparencymarketresearch.com